A-Book vs B-Book vs Hybrid Models: Technical Implementation Guide

The Execution Decision That Defines Your Brokerage

Every forex broker eventually faces the same question: what do we do with client orders?

The answer determines your revenue model, your risk profile, your LP relationships, your technology stack, and — if you get it wrong — whether you’re still in business after the next flash crash. We’ve seen brokers blow up from poor a-book b-book decisions. The 2015 SNB event wiped out multiple A-book brokers who thought they had no market risk. Turns out, counterparty risk to LPs is still risk.

This guide is the technical deep-dive. We’re assuming you already understand the conceptual difference between A-book and B-book. If you don’t, read our Mastering Risk Management piece first. This one is for dealing desk managers, CTOs, and broker principals who need to actually implement these models — configure bridges, set exposure limits, build routing rules, and make the daily decisions that determine whether your brokerage prints money or hemorrhages it.

Fair warning: there’s no “best” model. A-book isn’t more ethical than B-book. B-book isn’t inherently predatory. Hybrid isn’t automatically superior. Each has trade-offs that depend on your capitalization, regulatory environment, client base, and risk appetite. Anyone telling you otherwise is selling something.

A-Book Execution: Technical Implementation

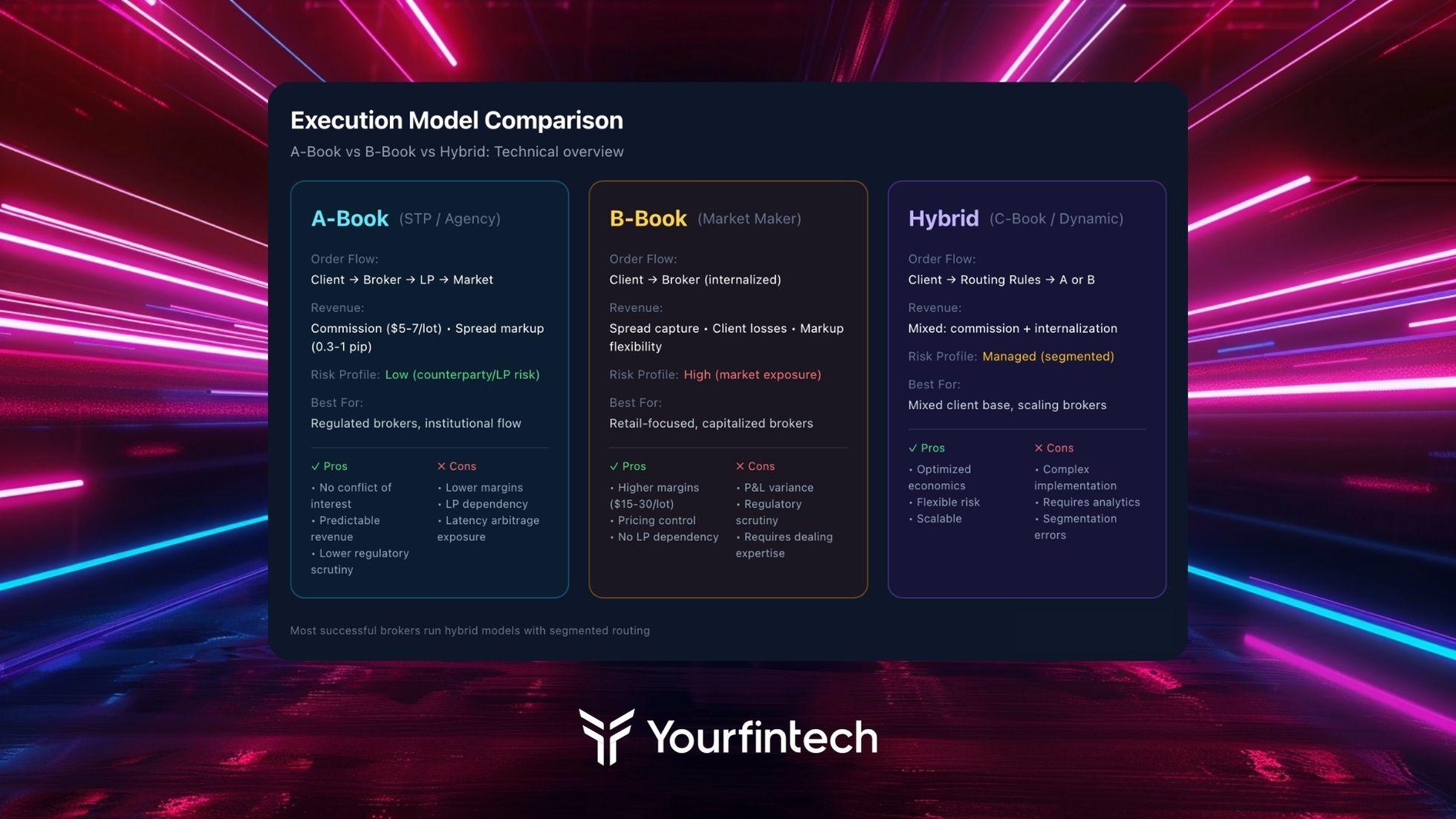

A-book — also called STP (Straight-Through Processing) or agency model — means passing client orders to external liquidity providers. You’re an intermediary, not a counterparty. Client wins, you still get paid. Client loses, you still get paid. Same spread markup or commission either way.

Sounds simple. Implementation is not.

LP Connectivity and Aggregation

Pure A-book requires reliable liquidity provider connections. This isn’t one LP and a prayer. Serious A-book operations aggregate quotes from multiple sources — typically 3-8 LPs — and route orders based on best available price.

Bridge configuration matters enormously here. Your liquidity bridge (oneZero, PrimeXM, Centroid, FXCubic, or similar) handles:

- Price aggregation from multiple LP feeds

- Best bid/offer compilation

- Order routing and execution

- Position management and reporting

- Markup application

Latency is real. Independent tests in 2024 showed A-book brokers averaged execution speeds under 30 milliseconds. That’s fine for retail flow. For algorithmic traders exploiting latency arbitrage? They’ll eat you alive. This is why even “pure” A-book operations often have exceptions for certain client profiles.

Revenue Model: Commission vs Markup

A-book brokers make money two ways:

Commission per lot: Transparent, typically $5-7 per standard lot round-turn. Client sees raw spreads from LP feed plus explicit commission. ECN-style accounts use this model.

Spread markup: Broker adds 0.3-1.0 pip to LP spreads before showing to client. No separate commission line item. Client sees “all-in” spread. Most STP accounts use this.

The math on commission: if you’re charging $6/lot and your average client trades 10 lots/month, that’s $60/month revenue per active trader. If LP costs run $2-3/lot, your gross margin is around $3-4/lot. You need volume to make A-book work.

Spread markup math depends on client flow patterns and LP pricing. Mark up 0.5 pip on EUR/USD with average trade size of 0.5 lots? That’s roughly $2.50 per trade. Volume still matters, but per-trade economics can be slightly better.

A-Book Risk: It’s Not Zero

The “no risk” framing of A-book is misleading.

You face counterparty risk to LPs. If your LP goes bust mid-trade, you’re exposed. You face execution risk — client orders rejected by LP still need filling. You face gap risk during fast markets when LP quotes disappear. And you face the latency arbitrage problem mentioned above.

The SNB event in January 2015 destroyed multiple A-book brokers. They had matched positions with LPs who couldn’t honor fills when CHF moved 30% in minutes. “Hedged” positions weren’t hedged when counterparties failed.

Real A-book risk management means: multiple LP relationships, careful credit limit monitoring, rejection handling protocols, and — ironically — sometimes internalizing flow during extreme volatility when LP quotes become unreliable.

B-Book Execution: Technical Implementation

B-book — also called internalization or market-making — means taking the other side of client trades. Client buys EUR/USD, you sell EUR/USD. Your P&L is inversely correlated with client P&L.

This sounds predatory when explained badly. Here’s the reality: the majority of retail forex traders lose money. Industry data consistently shows 70-80% of retail CFD/forex accounts are unprofitable. If you internalize that flow, you’re statistically likely to profit. Not guaranteed — individual clients can and do win — but probable in aggregate over time.

That said, B-book without proper risk management is how brokers blow up. One profitable trader with size can create massive exposure. The dealing desk exists to manage this.

Exposure Management

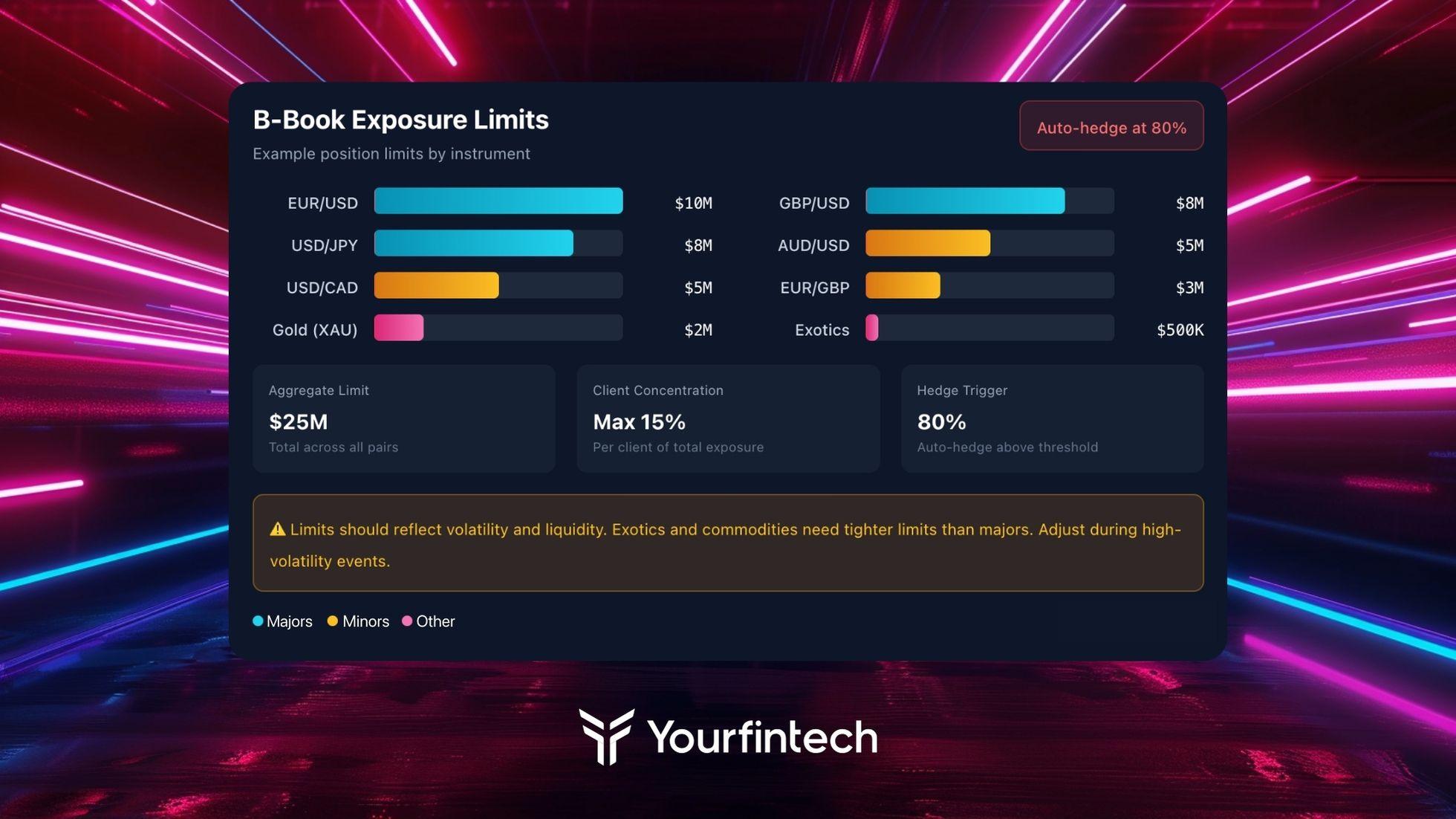

B-book risk management centers on exposure limits. You need to know — in real-time — your net position across all instruments and all clients.

Position limits by currency: Set maximum net exposure per currency pair. EUR/USD might tolerate $10M net position. TRY/JPY? Maybe $500K. Volatility and liquidity determine appropriate limits.

Position limits overall: Aggregate exposure across all pairs, measured in base currency equivalent. This catches situations where you’re long EUR across multiple pairs simultaneously.

Client concentration limits: No single client should represent more than X% of your total exposure. One whale shouldn’t determine whether your month is profitable.

When exposure approaches limits, you hedge. This is where B-book and A-book blur — a “B-book” broker hedging excess exposure is functionally doing A-book execution for that portion of flow.

Pricing Control

B-book brokers control their own pricing. You’re not obligated to show LP prices — you’re making a market.

This means you can offer fixed spreads (useful for marketing, dangerous during volatility), widen spreads during news events, or adjust pricing based on exposure. If you’re massively long EUR/USD from client sells, you might tighten the offer to attract buyers and balance your book.

Pricing manipulation for profit — showing worse prices to winning clients, for example — is a different matter. Regulated brokers are prohibited from this. But adjusting spreads based on market conditions and exposure is standard market-making practice.

The Dealing Desk Function

Active B-book operations typically have dealers monitoring positions in real-time. Their job:

- Monitor net exposure by instrument and overall

- Decide when to hedge excess positions

- Adjust pricing parameters based on conditions

- Flag unusual client activity (potential toxic flow)

- Manage execution during high-volatility events

Automated dealing is increasingly common — algorithms handle routine exposure management, with human oversight for exceptions. But fully automated B-book without experienced dealers monitoring is risky. Markets do unexpected things, and algorithms designed for normal conditions can fail spectacularly during crises.

B-Book Revenue and Risk Math

B-book revenue per lot is significantly higher than A-book — often $15-30+ depending on client loss rates and spread capture. But variance is also higher. A good month might see 80% of internalized flow unprofitable (for clients). A bad month — maybe after a major trend move that caught clients on the right side — might see 60% profitable.

Risk management tools like Value at Risk (VAR) help quantify exposure, but practical daily limits work better in live operations. Simple position limits with automatic hedging triggers are more reliable than sophisticated models that fail during exactly the conditions when you need them most.

Hybrid Execution: Technical Implementation

Hybrid — sometimes called C-book — combines A-book and B-book based on client characteristics, trade characteristics, or market conditions. This is what most successful mid-to-large brokers actually run.

The core idea: internalize flow likely to be unprofitable (for clients), externalize flow likely to be profitable. Keep the statistical edge, offload the risk from traders who might actually win.

Client Segmentation Rules

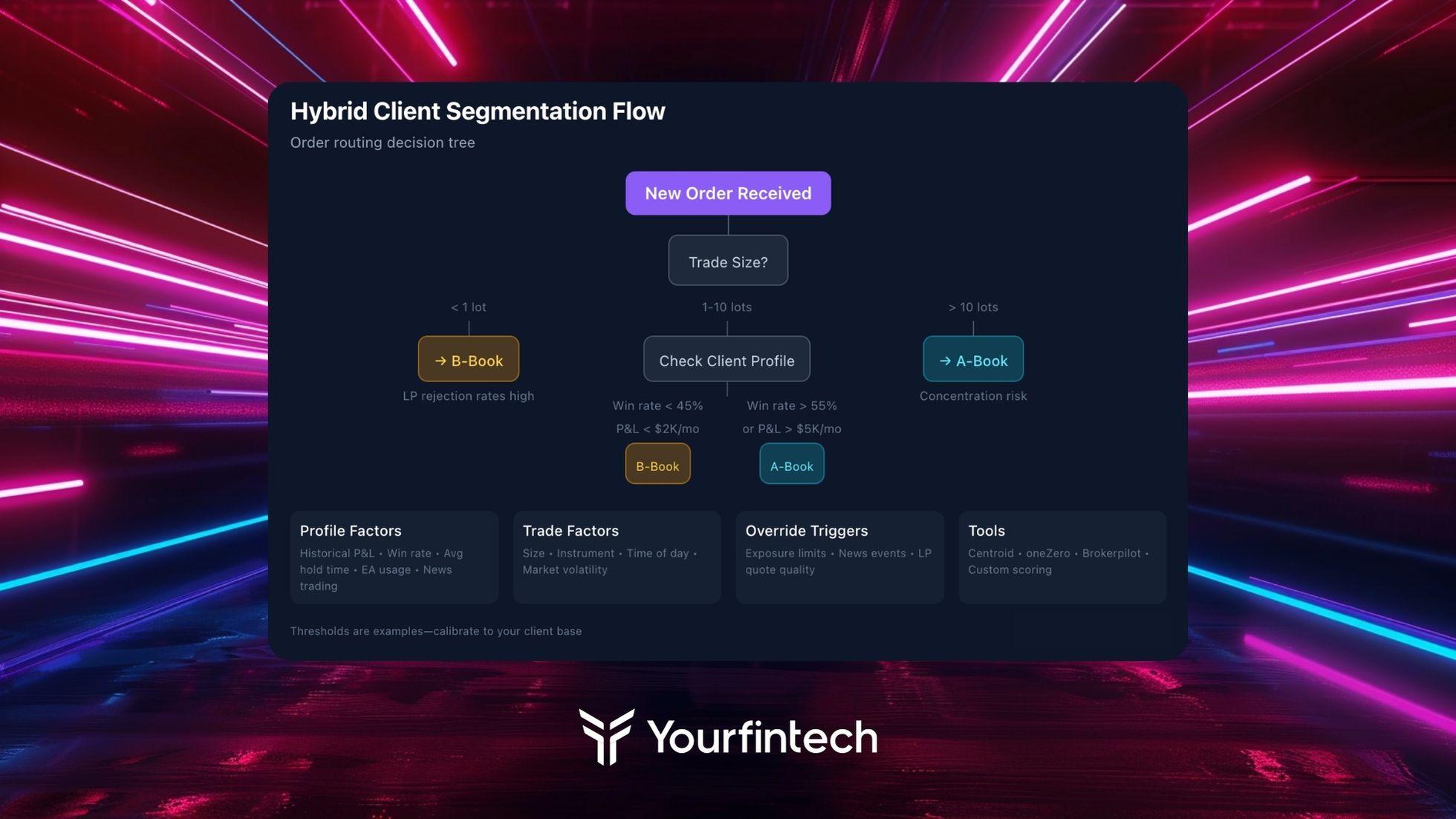

Hybrid execution requires routing logic. How do you decide which trades go to A-book vs B-book?

Profile-based routing: Segment clients by historical profitability, trading style, and risk characteristics. New clients with small deposits and no track record? B-book. Client with $50K deposit, 6-month history of consistent profits, trades around news events? A-book.

Segmentation criteria typically include:

- Account equity and deposit history

- Historical P&L (rolling 30/60/90 days)

- Trading frequency and average hold time

- Use of EAs/algorithms

- Trading around high-impact news

- Win rate and average winner/loser ratio

- Leverage utilization

Brokers use risk management platforms (Brokerpilot, Centroid’s analytics, proprietary systems) to score clients and automate routing decisions. The scoring models improve over time as you accumulate data on which characteristics predict profitability.

Trade-Based Routing

Beyond client profiles, individual trade characteristics can trigger routing decisions:

Trade size: Small trades (under 1 lot) might always internalize regardless of client profile — LP rejection rates on small orders are high anyway. Large trades (over 10 lots) might always externalize to avoid concentration risk.

Instrument: Majors with tight spreads and deep liquidity internalize well. Exotics with wide spreads and thin liquidity might always A-book — the risk/reward on internalizing illiquid pairs isn’t favorable.

Market conditions: During NFP or FOMC announcements, LP quotes become unreliable. Some hybrid systems automatically switch to B-book during defined high-volatility windows, then revert to normal routing after.

Dynamic Switching

Sophisticated hybrid systems adjust routing in real-time based on:

- Current exposure levels (approaching limits → more A-book)

- Market volatility (VIX spike → routing changes)

- Client behavior patterns (unusual activity → flag for review)

- LP quote quality (wide spreads or slow response → internalize)

AI and machine learning are entering this space. Leading brokers use predictive models to anticipate which clients are becoming profitable before it shows in raw P&L numbers. Trade pattern changes, strategy shifts, improved risk management — these can signal a client transitioning from losing to winning.

Whether the ML hype delivers on promises is another question. Most brokers we work with still rely primarily on rule-based systems with human oversight, using analytics for insight rather than fully automated decision-making.

Bridge Configuration: The Technical Heart of Execution

Your liquidity bridge is where execution models become operational reality. Configuration decisions here directly impact every aspect of trading — pricing, execution speed, risk management, and revenue.

Bridge Selection

Major options for MT4/MT5 brokers:

Centroid: Deep risk management features, granular A/B-book routing, strong analytics. Best for established brokerages with active dealing desks. Higher cost and setup complexity.

oneZero: Institutional-grade execution management. Hub-to-Hub connectivity, flow analytics, LP benchmarking. Best for large brokerages, prime-of-primes, and market makers. More infrastructure than most sub-enterprise brokers need.

PrimeXM: Solid mid-market option with good LP connectivity. XCore aggregation engine handles multi-LP setups well. Reasonable balance of features and cost.

FXCubic: Competitive pricing, good MT4/MT5 integration. Accessible to growing brokerages. Less feature depth than Centroid/oneZero but covers core needs.

Bridge choice depends on your execution model complexity. Pure A-book with one LP? Almost any bridge works. Hybrid with dynamic routing, multiple LP tiers, and real-time analytics? You need the more sophisticated options.

Key Configuration Parameters

Regardless of bridge, you’ll configure:

LP priority and routing: Primary LP, secondary fallback, rejection handling. Do rejected orders retry with secondary LP or return to client?

Markup rules: Spread markup by instrument, by client group, by time of day. Different markups for different account types.

Execution type: Market execution vs instant execution. Virtual dealer delays (be careful — regulators scrutinize artificial delays).

Hedging parameters: Auto-hedge triggers, hedge ratios, hedge LP selection. Partial hedging vs full hedging.

Exposure limits: Per-symbol limits, aggregate limits, client concentration limits. Alert thresholds vs hard limits.

Document everything. Regulators increasingly want to see execution policies and how systems implement them. “The bridge handles it” isn’t sufficient documentation.

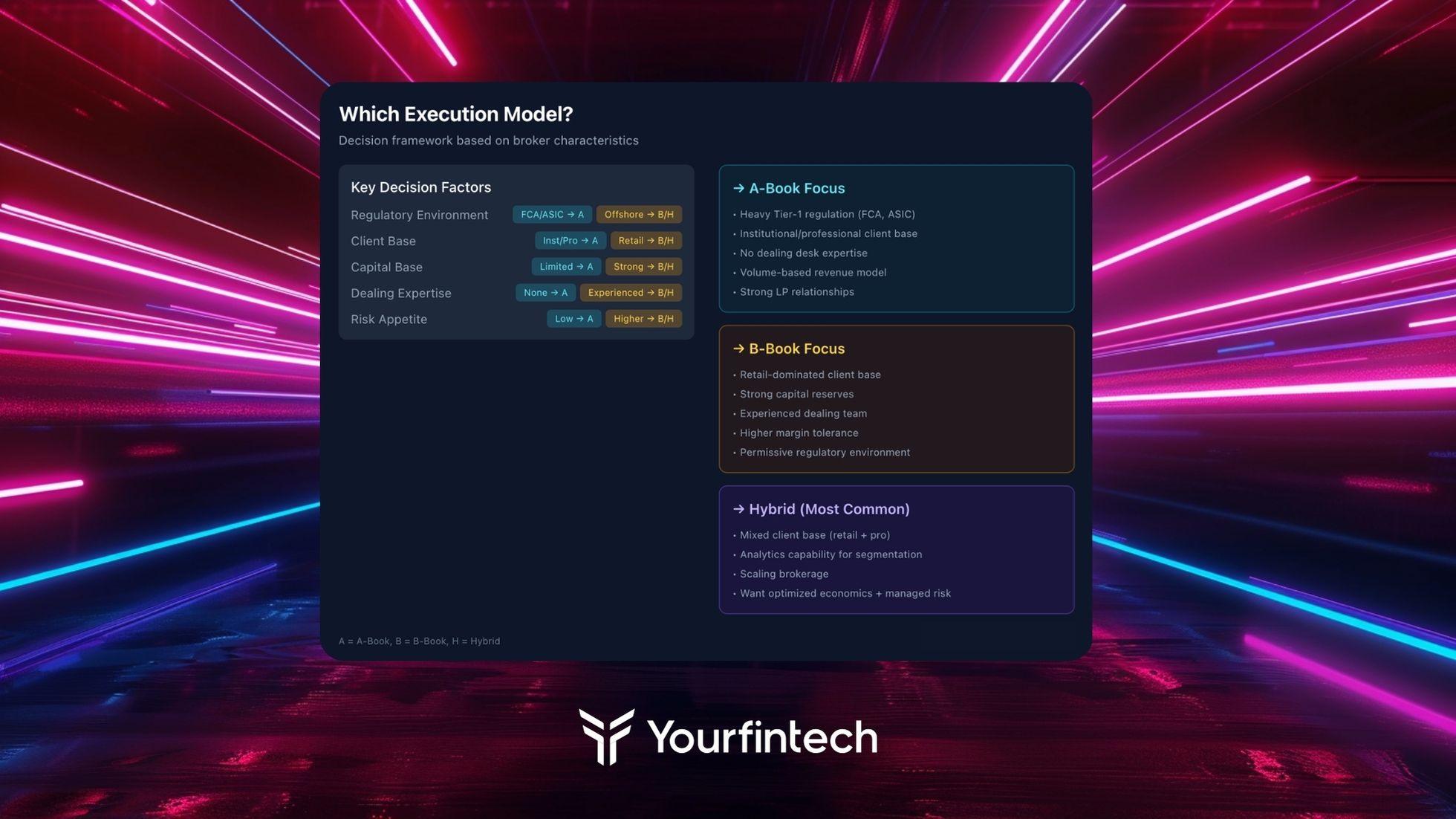

Practical Decision Framework: When A-Book, when B-Book

After all the technical detail, the question remains: what should your brokerage actually do?

Pure A-Book Makes Sense When:

- You’re heavily regulated (FCA, ASIC) with intense execution scrutiny

- Your client base is predominantly professional/institutional

- You lack dealing desk expertise or don’t want the operational complexity

- You’re okay with lower per-trade margins and need volume to compensate

- Your LP relationships are strong with reliable execution

B-Book Focus Makes Sense When:

- You have dealing desk expertise and risk management infrastructure

- Your client base is predominantly retail with typical loss patterns

- You have capital to absorb variance in monthly P&L

- You want higher per-trade margins and can manage the risk

- Regulatory environment permits market-making models

Hybrid Is Appropriate When:

- You have mixed client base (retail + semi-pro + professional)

- You want to capture B-book economics without unlimited risk

- You have technology and analytics to segment clients effectively

- You’re scaling and need flexibility as client mix evolves

- You want to A-book toxic flow while retaining profitable internalization

Most brokers we work with at YourFintech end up running hybrid models. The pure plays — 100% A-book or 100% B-book — are increasingly rare outside specific niches. The economics and risk management of hybrid execution, when implemented properly, outperform either extreme.

Common Implementation Mistakes

After years of working with broker dealing desks, here’s what goes wrong:

Undercapitalized B-book: You need capital to absorb variance. A few winning clients in a row shouldn’t threaten your solvency. If B-book P&L swings give you existential anxiety, you’re undercapitalized for the model.

Poor client segmentation: Routing all flow the same way defeats the purpose of hybrid. Invest in analytics. Know your clients.

LP concentration: Single LP dependency is dangerous. When that LP has issues — and they will — your entire execution fails. Minimum two LPs, preferably more.

Ignoring toxic flow signals: Latency arbitrage, news straddles, scalping on slow quotes — these patterns are identifiable. Route them to A-book or reject them. Don’t internalize flow that’s structurally likely to win.

Inadequate documentation: Regulators want execution policies. If your policy says one thing and your bridge does another, you have a compliance problem.

Over-automating too early: Automated dealing is powerful but requires tuning. Start with human oversight, understand your flow patterns, then automate incrementally.

Conclusion

A-book, B-book, and hybrid aren’t moral categories. They’re execution models with different risk/return profiles and operational requirements.

A-book transfers risk to LPs in exchange for lower per-trade economics and execution dependency. B-book internalizes risk for higher margins and pricing control, requiring capital and dealing expertise. Hybrid combines both, using client segmentation to optimize the mix.

The “right” model depends on your specific situation — regulation, capitalization, client base, and operational capabilities. Most successful brokerages end up running hybrid execution with sophisticated routing rules, because pure plays leave either money or risk management on the table.

Implementation is where theory meets reality. Bridge configuration, exposure limits, segmentation rules, LP relationships — these technical decisions determine whether your execution model works as intended or creates problems you didn’t anticipate.

Get the technical foundation right. The business model follows.

Recent Articles

Liquidity Bridge Technology: Connecting Your Broker to Multiple Providers

13.01.26

The forex market moves $9.6 trillion daily. That number from the Bank for International Settlements still catches us off guard sometimes — it’s roughly 25 times the daily volume of all global stock markets combined. At YourFintech, we’ve spent years helping brokers navigate this enormous flow, and one thing has become abundantly clear: the infrastructure […]

Mastering Risk Management for Sustainable Profit

11.11.25

Every broker’s primary goal is to maximize revenue while maintaining a sustainable risk framework. Yet, despite the abundance of experience in the market, many brokers still overlook the fundamentals of proper risk management. Understanding how to manage exposure, structure a brokerage efficiently, and select the right operational model – market maker, agency, or hybrid – […]

Two Metrics Every Prop Firm Must Master

01.07.25

Two Metrics Every Prop Firm Must Master What separates thriving prop trading firms from those that crumble under market pressure? It’s not just about recruiting the best prop traders or having the most advanced trading tools. The real secret lies in two critical financial metrics that most proprietary trading firms either ignore or misunderstand entirely. […]

Global Forex Broker Licensing Requirements: Jurisdiction Comparison 2026

19.02.26

Why Your Forex Broker License Choice Matters We get asked about forex broker license options more than almost anything else at YourFintech. “Should I go CySEC or offshore?” “Is an FCA forex broker license worth it?” “What about Vanuatu?” And honestly, most of the time the question is backwards. People pick a jurisdiction first, then […]

Trader Segmentation & Risk Triggers – A Quick Breakdown

17.06.25

Trader Segmentation & Risk Triggers – A Quick Breakdown Do you really know what’s driving your brokerage’s revenue and what’s threatening it? Are your most active traders actually your biggest risk exposure? Every day, brokers face a fundamental challenge: distinguishing between traders who generate sustainable revenue and those who pose hidden threats to their operations. […]

Forex Broker Risk Management: Essential Strategies + Prop Firms Included

05.01.26

Understanding the Forex Broker Risk Management Landscape Between 80 and 100 proprietary trading firms collapsed in 2024, and forex broker risk management – or the lack of it – wasn’t the simple explanation everyone expected. At YourFintech, we spent three weeks analyzing these failures, expecting to find the usual suspects: inadequate capital, poor technology, inexperienced […]

How Do Liquidity Providers Work? Guide for Forex Brokers and Prop Firms

01.02.26

Here’s something that still surprises us at YourFintech: brokers will spend months choosing a trading platform, weeks negotiating payment processor fees, and maybe an afternoon picking their liquidity providers. Then they wonder why execution quality is inconsistent. Liquidity providers are the pricing infrastructure. Everything else — the slick UI, the client portal, the marketing — […]

The Strategic Value of Consistency Rules in Prop Trading Evaluations

01.07.25

The Strategic Value of Consistency Rules in Prop Trading Evaluations You’re a promising trader with a killer strategy, stellar technical analysis skills, and the confidence to take on the financial markets. You’ve just landed an interview with the best prop firm, but there’s one thing standing between you and that desired funded account: consistency rules […]